● Market Intelligence Report

Loading...

NO. OF PAGES

259

FORECAST PERIOD

2026 – 2031

BASE YEAR

2025

FORMAT

PDF + Excel

UPDATED

About this report

The Global Floating Production Systems (FPS) Market is sized at around USD 41 billion in the year 2025. It plays a vital role in the development of offshore crude oil and natural gas resources, with the capability of working in deep water and ultra deep water environments where conventional platforms cannot operate.

Market growth is fueled by continued investment of capital in offshore, the sanction of deep water projects, as well as the continued demand for energy security, especially in South America and West Africa geographic regions.

However, investment discipline, aging fleets, regulation, and pricing pressures due to global asset surplus impact the market. Despite the challenges, technological standardization, redeployment, and competitive project economics continue to sustain the FPS market's steady growth.

Market Definition

The Global Floating Production Systems (FPS) Market refers to the market for offshore facilities used to process hydrocarbons at sea, particularly in deep water and ultra deep water environments where fixed platforms are uneconomic.

FPS solutions include FPSOs (Floating Production, Storage and Offloading units), semi-submersible production platforms, and Tension Leg Platform (TLP).

Key players operating across FPS ownership, engineering, construction, and operations include Transocean Ltd., Samsung Heavy Industries, SBM Offshore, BW Offshore, Bumi Armada, and Hyundai Heavy Industries, which together dominate global FPS development and operations.

Market Dynamics

Drivers

Sustained Offshore Capital Allocation Despite Energy Transition

Despite stepped-up policy support to accelerate the energy transition, significant and continuing investment flows are seen to go into offshore oil and gas projects in 2026. Due to their security of supply, long lead times, and competitive costs.

Global upstream investment continued to top USD 520 billion in 2025, with offshore operations representing a notable percentage of long-cycle investments, as they offer large, steady volumes over a lifespan of 20-30 years to offset natural decline from mature onshore fields.

Additionally, assets in the deep water and ultra deep water segment have proven to be rather resilient. Many sanctioned offshore projects exhibit breakeven prices in the USD 35-45 per barrel range, which is enough to prove that these projects have some level of economic viability, even when the crude oil price estimate is rather conservative.

Furthermore, exploration in 2026 is marked by sustained capital discipline, with global spending expected to hold steady at just over USD 60 billion. There is an anticipation that more than 60 offshore frontier wells will be drilled in 2026, primarily across the Asia Pacific, Africa, and South America.

While capital discipline remains evident, investment is increasingly concentrated in projects with strong cost competitiveness and scalable production models. The combination of improved project economics, long-life reserves, and continued strategic offshore development reinforces sustained capital allocation into floating production systems through 2026.

A notable instance is ExxonMobil’s USD 2.32 billion FPSO acquisition in Guyana in February 2026, highlighting sustained operator confidence in floating production infrastructure. Guyana has emerged as a major deep water growth province, supported by multiple high-capacity FPSOs delivering long-term production stability.

From a supply side perspective, offshore production is increasingly driving global output stability. In the key regions of the Gulf of Mexico in the United States, Brazil, and West Africa, offshore fields are increasingly contributing to the rising share of non-OPEC incremental supply growth in 2026.

These regions have relied on a floating production system for their production. These systems have helped operators monetize their discoveries without the need for fixed infrastructure.

Restraint

Global Market Oversupply and Gloomy Pricing

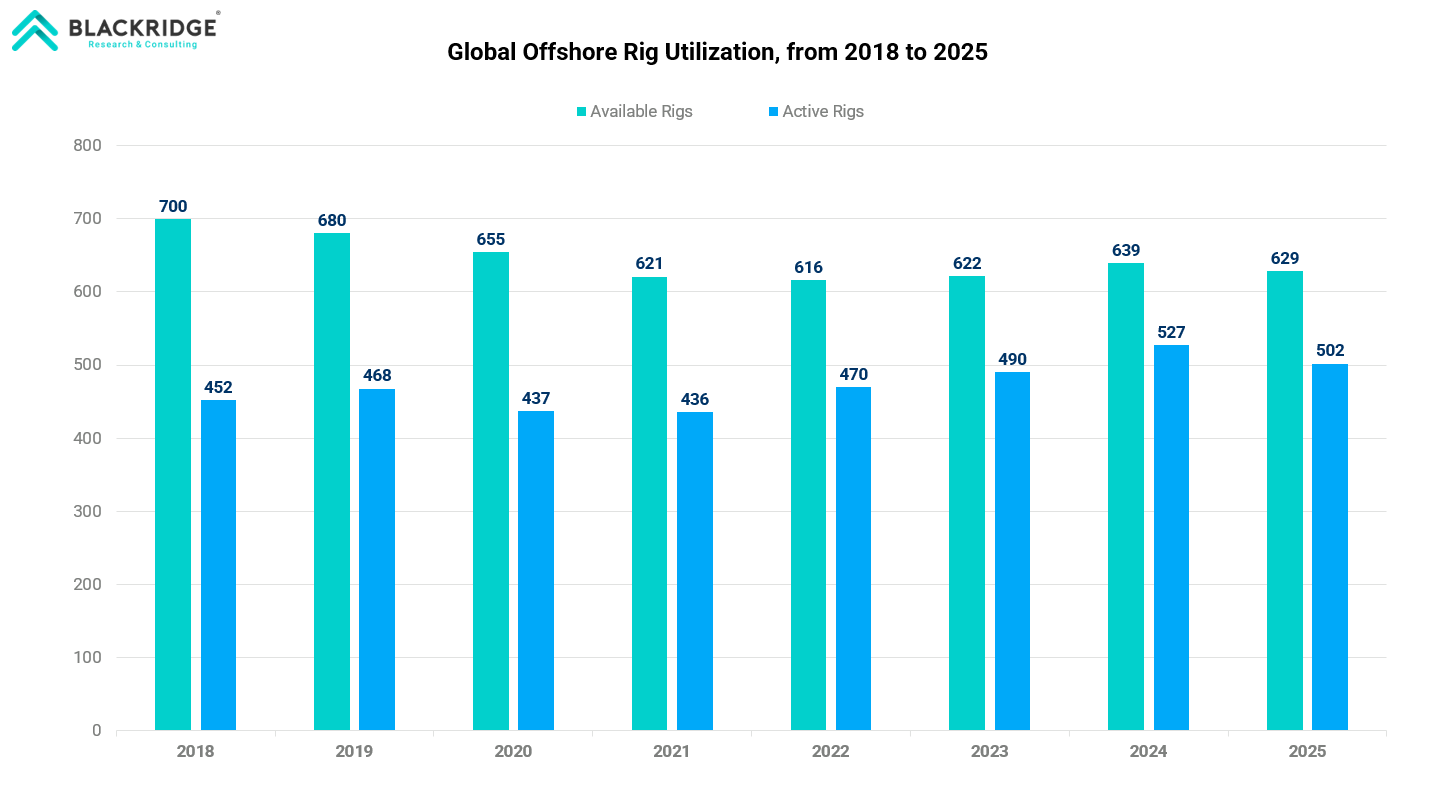

The offshore oil and gas service market continues to face oversupply and pricing challenges in the year 2025. Demand for offshore services has stabilized; however, the number of offshore drilling support units globally continues to outstrip sustainable demand, especially in the mature markets and secondaries.

A material number of rigs continue to sit idle or in stack, which keeps the supply side competitive and the prices under pressure.

Many rigs remain idle or stacked, keeping overall supply high and competition strong. This excess capacity limits dayrate recovery and prevents pricing from returning to previous peak levels.

In many cases, contractors reduce rates to win contracts, often covering only operating and capital costs with limited margin upside.

Regional variations further influence pricing dynamics. Markets such as Brazil and the U.S. Gulf of Mexico show tightening conditions for high-specification units, while other regions continue to face excess availability.

Because offshore rigs are mobile, units released from tighter markets can relocate to softer regions, increasing competition and moderating global rate improvement.

Tightening supplies are seen in regions such as Brazil and the U.S. Gulf of Mexico; the U.S. offshore fleet decreased by four units to 94 rigs, resulting in a reduction of approximately 4.08% in 2025.

Although fleet rationalization through scrappage has reduced the total number of offshore rigs, the reactivation of stacked semi-submersible units in response to incremental demand continues to offset capacity reductions, thereby delaying a meaningful tightening of the global offshore supply balance and limiting the need for newbuilds.

Uncertainty and careful capital allocation in the macroeconomic scenario aggravate the above impacts. The emphasis on short-term contracts and cost minimization makes the contract duration and price in the offshore services market shorter.

Market Segmentation

By Facility Type

The offshore market can be segmented in terms of facility types. This is largely driven by differences in their applications, costs, and operating environments. FPSOs (Floating Production, Storage and Offloading units) dominate the offshore market and approximately 70% of global floating offshore production capacity.

This dominance is driven by their ability to operate in deep water and ultra deep water fields in the absence of a pipeline system. Their flexibility, coupled with a long operating life, makes them the perfect option for regions such as Brazil, West Africa, and Guyana.

The semi-submersible production platform is mainly used for operations under harsh conditions, especially in the North Sea, where platform stability under critical operating conditions is essential. Although fewer in number, they are more expensive per unit due to structural complexity.

Tension Leg Platforms (TLP) are the most restricted category. Its usage is confined to particular deep water environments. Its high installation and foundation costs are also major drawbacks.

Despite their smaller numbers, semi-submersible platforms and TLPs together account for approximately 30% of offshore floating production activity, underscoring their strategic importance. The day rates of the vessels are high compared to the FPSOs.

By Region

The Global Floating Production Systems (FPS) market is segmented by region based on offshore resource potential, water depth, and development intensity.

South America represents the largest regional segment, led by Brazil’s deep water and ultra deep water pre-salt fields. It leads high-end offshore activity, holding 43.2% of contracted drillships in global share.

The region accounts for a substantial share of global FPS installations, with most new offshore developments relying on high-capacity FPSOs to support long-life production.

In contrast, Europe represents a more mature offshore market, dominated by the North Sea, where FPS deployment is focused on field life extension and redevelopment of mature assets rather than large greenfield projects. Floating units are selectively used to maximize recovery from aging fields.

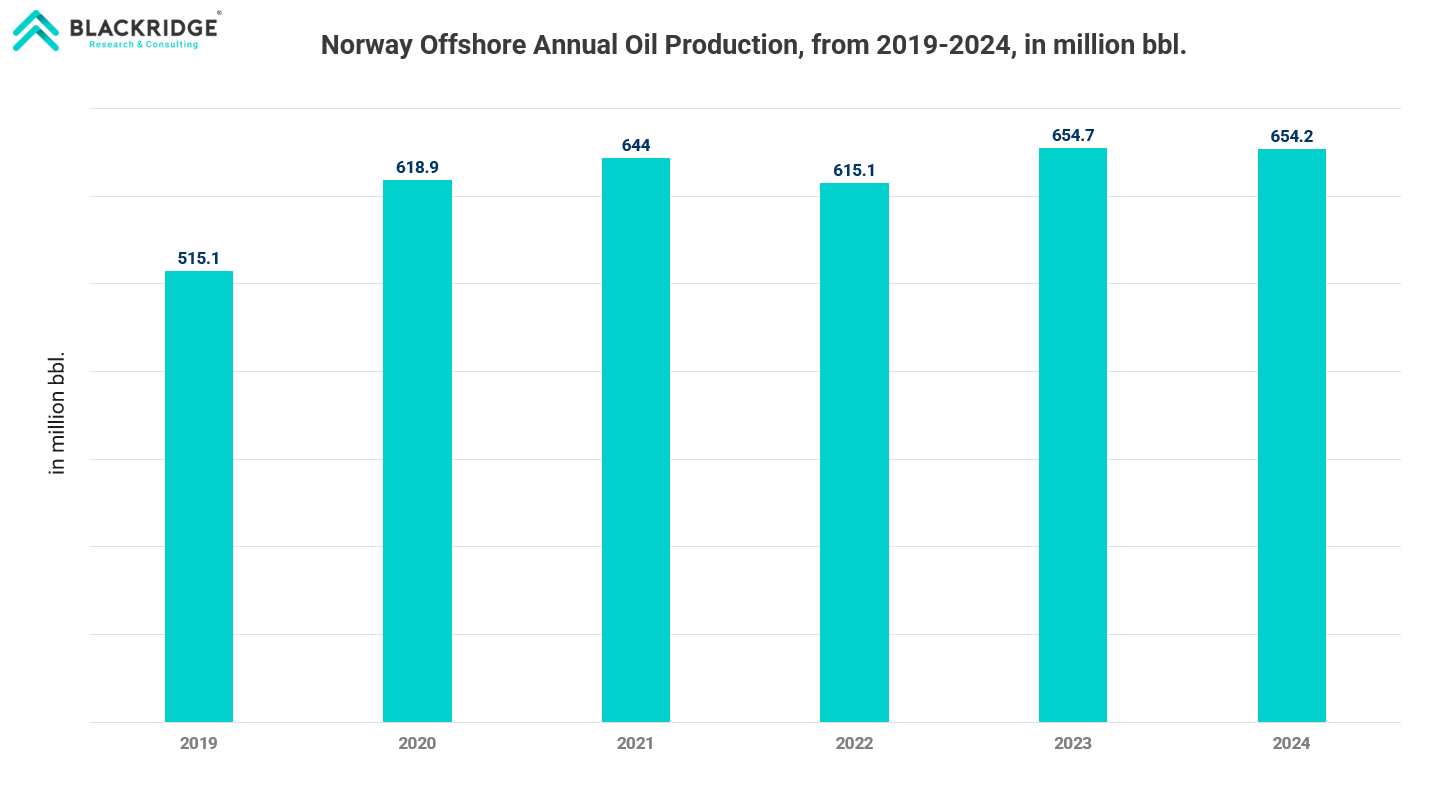

The North Sea dominates with harsh-environment activity, accounting for 37.5% of the active global semisubmersible fleet, with Norway serving as the key regional driver.

Market Opportunity

The global Floating Production Systems (FPS) market is entering a pivotal phase, driven by a surge in deep water and LNG-linked final investment decisions (FIDs) expected to build through 2026 and intensify by 2027.

West Africa represents a primary market opportunity, emerging as a critical horizon for new global Floating Production Storage and Offloading (FPSO) developments. The region is a vital component of the Golden Triangle of Brazil, Guyana, and West Africa, currently accounting for 14.9% of the global contracted drillship fleet, a strong precursor to production infrastructure needs.

The region hosts a large portfolio of undeveloped and partially developed offshore discoveries in water depths exceeding 1,000 meters, making FPSOs the most practical and cost-effective production option.

Over 60 offshore frontier wells are anticipated globally in 2026, with a heavy focus on Africa. Due to this, Namibia has gained status as an offshore giant, while established markets like Angola continue to see high-specification unit deployments.

FPS units are the optimal solution for these areas because they can process and store hydrocarbons in remote deep water environments where pipeline infrastructure is nonexistent. This flexibility makes them essential for developing the marginal and frontier fields that define the West African offshore landscape.

Market Trends and Developments

New FPS projects in 2026 are incorporating lower-carbon designs, including electrification readiness, improved gas handling, and energy efficiency upgrades, aligning FPS developments with corporate decarbonization goals.

The market is increasingly targeting remote deep water areas without pipeline infrastructure, where FPSOs remain the preferred solution for marginal fields. In parallel, new production systems are closely linked to the transition towards LNG, with 2026 expected to mark a ramp-up in floating supply capacity.

In May 2025, BW Offshore completed the acquisition of the FPSO Nganhurra, a lay-up unit from Malaysia, to reposition it for future deployment. This strategic move strengthens BW Offshore’s fleet and reflects market activity in secondary FPSO markets.

In September 2025, Carlyle agreed to acquire the entire Floating Production, Storage and Offloading (FPSO) business from Altera Infrastructure for an undisclosed amount. The acquired business includes Altera’s full FPSO portfolio, the FSO Yamoussoukro, and the 50% ownership in the Joint Venture Altera&Ocyan.

In November 2025, ADES finalized the acquisition of Shelf Drilling, creating a combined platform of 83 offshore units and 40 onshore rigs operating across 19 countries. The enlarged fleet includes 46 premium jackups plus other offshore assets.

In January 2026, Brazilian company Brava Energia completed the acquisition of Petronas’ 50% non-operating stakes in the Tartaruga Verde and Espadarte Module III offshore assets. The deal is valued at USD 450 million.

The new report from Blackridge Research on the Global Floating Production Systems (FPS) Market comprehensively analyzes the Market and provides deep insight into the current and future state of the industry.

The study examines the drivers, restraints, and regional trends influencing the Global Floating Production Systems (FPS) Market demand and growth.

The report also addresses present and future market opportunities, market trends in the Global Floating Production Systems (FPS) Market, important commercial developments, regions, and segments poised for fastest growth, competitive landscape, and market share of key players.

Further, the report will also provide the Global Floating Production Systems (FPS) Market size, demand forecast, and growth rates.

What do we cover in the report?

Global Floating Production Systems (FPS) Market Drivers & Restraints

The study covers all the major underlying forces that help the market develop and grow, and the factors that constrain the growth.

The report includes a meticulous analysis of each factor, explaining the relevant qualitative information with supporting data.

Each factor's respective impact in the near, medium, and long term will be covered using the Harvey balls for visual communication of qualitative information and functions as a guide for you to analyze the degree of impact.

Global Floating Production Systems (FPS) Market Analysis

This report discusses the overview of the market, latest updates, important commercial developments, structural trends, and government policies and regulations.

This section provides an assessment of the Global Floating Production Systems (FPS) Market demand.

Global Floating Production Systems (FPS) Market Size and Demand Forecast

The report provides the Global Floating Production Systems (FPS) Market size and demand forecast until 2031, including year-on-year (YoY) growth rates and CAGR.

Global Floating Production Systems (FPS) Market Analysis

The report examines the critical elements of the Global Floating Production Systems (FPS) Market supply chain, its structure, and participants

Using Porter's five forces framework, the report covers the assessment of the Global Floating Production Systems (FPS) Market state of competition and profitability.

Global Floating Production Systems (FPS) Market Segmentation & Forecast

The report dissects the Global Floating Production Systems (FPS) Market into various segments. A detailed summary of the current scenario, recent developments, and market outlook will be provided for each segment.

Further, market size and demand forecasts will be presented along with various drivers and barriers for individual market segments.

Effective market segmentation enables you to identify emerging trends and opportunities for long-term growth. Contact us for a "bespoke" market segmentation to better align the research report with your requirements.

Regional Market Analysis

The report covers detailed profiles of major countries across the world. Each country's analysis covers the current market scenario, market drivers, government policies & regulations, and market outlook.

In addition, market size, demand forecast, and growth rates will be provided for all regions.

The following are the notable countries covered under each region.

North America - United States, Canada, Mexico, and the rest of North America

South America - Brazil, Argentina, and the rest of South America & Latin America

Europe - Russia, Norway, the United Kingdom (UK), and the rest of Europe

Asia Pacific - China, India, Japan, South Korea, Australia, Rest of APAC

Rest of the world - Nigeria, South Africa,, and other countries

Key Company Profiles

This report presents detailed profiles of Key companies in the Global Floating Production Systems (FPS) industry, such as Transocean Ltd., Samsung Heavy Industries, SBM Offshore, BW Offshore, Bumi Armada, Hyundai Heavy Industries, and more. In general, each company profile includes an overview of the company, relevant products and services, a financial overview, and recent developments.

Competitive Landscape

The report provides a comprehensive list of notable companies in the market, including mergers and acquisitions (M&As), joint ventures (JVs), partnerships, collaborations, and other business agreements.

The study also discusses the strategies adopted by leading players in the industry.

Executive Summary

The Executive Summary will be jam-packed with charts, infographics, and forecasts. This chapter summarizes the findings of the report crisply and clearly.

The report begins with an Executive Summary chapter and ends with Conclusions and Recommendations.

Get a free sample copy of the Global Floating Production Systems (FPS) Market report by clicking the "Download a Free Sample Now!" button at the top of the page.

Table of Contents

Report Details

This report helps to

Who needs this report?

What's included

Why buy this report?

Want to know about Current Offers?

Methodology

Multi-stage process combining primary C-suite interviews and field engineer surveys with comprehensive secondary data triangulation across company filings, government statistics, and trade databases.

Secondary Research

Discussion Guides

Primary Research

Data Triangulation

Market Engineering

Data Validation

Report Writing

Common Questions

Single User License

The Single User License will provide access to only one user.

Team License

The Team License will provide access only up to 7 users. This is great for a team.

Corporate License

This Premium package is ideal for large companies. By having Corporate license, any employee of your organization or its subsidiaries can access the report. You will also receive free industry update after six months and also a white label powerpoint presentation.

Related Content

What people are saying about us

Haven’t found what you’re looking for?

More than 70% of our clients seek customized reports. Reach us out to get yours today!